Why you need it, and if you already have it, why you need to know what you’ve got!

Part 2: The inner workings of a policy: What to look for.

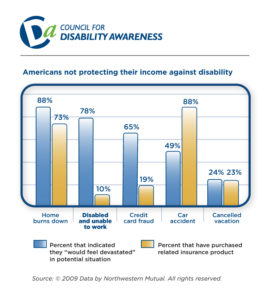

If you read my earlier piece on Disability Insurance entitled Part 1: Protecting Your Most Important Asset, then you probably understand the need to obtain Disability income coverage.

The next hurdle you may face is how to rate policies for your needs. Disability contracts are very complex; in fact, it can take a long time for an insurance professional to understand the ‘ins and outs’ of how policies function, so the average person with other things to do in their lives can certainly find the task overwhelming.

Here are a few items to consider:

1.) How much coverage do I need? A rule of Thumb is that you should have coverage of about 60-70% of your expenses to keep your current lifestyle. The reason for this 30 – 40% pay cut is because if you pay the premiums yourself, then the benefit is nontaxable, so no income taxes or FICA taxes will be taken from it. Also, many of your work-related expenses (i.e. – commuting or vehicle, eating out for lunch, retirement contributions, etc.) will no longer be needed either.

2.) How long after I am disabled will my coverage begin? This is referred to as the elimination period; think of it as an insurance deductible. In order for your premium to be lower, you may want to self-insure for a period of time before benefits begin, such as 90 or 180 days or even up to a full year. During this time, you can live off your emergency savings before the benefits start.

3.) When does the Insurance company consider me disabled and are there any exclusions? This is also known as the definition of disability. Ask your Insurance specialist to show you what the definition is from a sample or specimen contract. Also know if there are any accidents or illnesses excluded from the policy.

4.) If I cannot work in my particular specialty, am I covered? This is usually referred to as ‘own occupation’ and is most important in highly specialized fields, such as physical therapy, the surgical field or other highly specialized occupations.

The question is, will they still consider you disabled if you can do any work, but still can’t work your particular occupation in your specialized field? There are many policies that will pay a benefit if you can’t work in your true occupation for only 24 months, after that if you can work in ANY occupation, they would not consider you disabled and your benefits would end. In this situation, imagine a surgeon that required a steady hand, who had an injury or disease which made performing his tasks impossible. The policies that are not ‘true own occupation’ may only pay that surgeon for two years, but after that if he or she can answer phones at a desk, then they’re not considered disabled, and benefit payments would cease. This is an important design to watch out for.

5.) How long will my payments continue if I am disabled? Even with a true ‘own occupation’ definition as described above, many people may be unaware that their benefit period could be short, such as five years. If you were disabled for a lifetime at an early age, like in your late 30s or early 40s, benefits could cease long before retirement age. You may want to consider only policies that would guarantee benefits until age 65 or 67. Of course if you are only eligible for a shorter period; some coverage is better than no coverage, so get what you can.

6.) Residual and partial disability & COLA adjustments. What if you want to come back to work, but can’t work full time yet or can’t perform all of your job function. Most insurance companies try to encourage you to come back to work ASAP. And to help do this, there may be provisions in your policy choices that encourage going back to work without penalizing you by cutting benefits too soon. This is referred to as a residual or partial benefit; they can make up for lost wages from a decrease in duties performed or decrease in time worked.

Also important is having a cost of living adjustment (COLA). A $5,000 a month benefit may be right for today, but in ten or twenty years it may not be enough to pay your bills as inflation has eroded your purchasing power. Consider having a COLA of 3% or so built into the policy to battle inflation.

7.) The company’s financial Strength. Only choose a policy from a company that is rated financially strong. It is not a good idea to pay years of premiums to a financially weak company if they may not be around for you when you need them. Don’t save a few bucks now just to see an imperiled benefit in the future.

8.) Look to add a supplemental rider to the policy that helps save for retirement. Your policy may be well built including all the above provisions discussed above, but what about after benefits cease in your retirement years? Remember, if you become disabled, you likely are not able to put enough money into your retirement plans going forward. Generally, benefits are only about 60% of your previous income. If you are long term disabled, it is certainly possible that you will live a long life after retirement age, so what will you do for income at age 65 when benefits cease? You probably stopped contributions to your 401k long ago. The fact is you need to keep contributing to some type of retirement saving while you’re on benefit before age 65. There are some policies out there that will also pay into a type of trust that becomes available to you (or your beneficiaries) after age 65 that you can invest in mutual funds for long term growth. That’s how you can secure your later years, even in the event of long term disability!

For more information on how to protect you and your family, or for a review of the policy you have you can contact us HERE FOR HELP .

If you have Disability coverage through your work, then be sure to read Part 3 of my article Potential for serious gaps: group Disability through work